02.26.16

There was a continuing surge of investments and merger and acquisition (M&A) activity in branded natural and organic food & beverage companies in 2015, in addition to rapid growth in financings in the emerging world of foodtech, according to Nutrition Capital Network (NCN), an organization that connects investors with high-potential growth companies in the nutrition and health & wellness industry.

“2015 was a record year for equity investments and acquisitions in the nutrition and health & wellness industry, and by no small margin,” said Grant Ferrier, NCN founder and CEO. “Venture investments more than doubled in agtech, Branded Food & Beverages, and food delivery; in the latter two categories, more than one deal a week was announced.”

Increase In Earlier-Stage Investments

Interest from big food companies, venture and private equity funds, and “cross-over” investors from technology and biotech all helped drive activity, but Mr. Ferrier also noted an increase in earlier stage investments by high net worth individuals, angel investors, former industry executives, crowdfunding, incubators, accelerators and other alternative financing models. “In 2015 we counted 40 equity investments of less than $2 million in branded products, more than the previous two years combined.”

Equity Financings Rise 61%, M&As Increase 29%

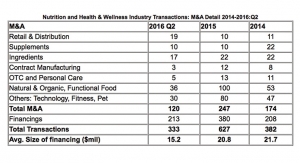

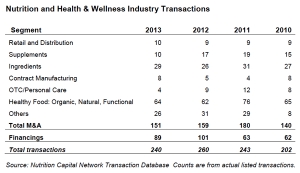

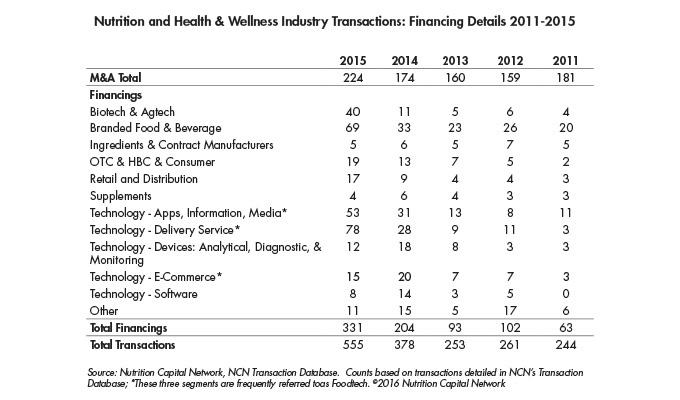

Overall transactions (i.e., acquisitions plus equity financings) in the nutrition and health & wellness industry totaled 558 in 2015, compared to annual totals of 382 in 2014 and 253 in 2013, according to the NCN Transaction Database, which tracks deals according to several industry segments, including supplements, natural & organic food, functional food, ingredients, retail & distribution, contract manufacturing, technology, natural personal care and household goods.

Equity financings accounted for 331 of total industry transactions in 2015, up 61% over the prior year, and more than $7 billion invested in deals for which the amount invested was available. Technology accounted for 207 or 63% of those equity financings but 69% of total value invested with 41 technology investments falling in the $50 million+ range.

Mergers and acquisitions (M&As) accounted for 224 of total industry transactions in 2015 compared to 168 in 2014, a 29% increase. Total transaction value of the top 10 listed deals in the food & beverage category was $7 billion.

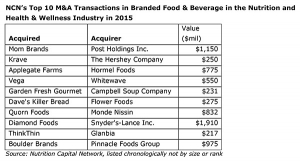

“Strong brands command a high price,” said Mr. Ferrier, citing Krave, Vega, Applegate Farms, Kettle and Smart Balance as examples of top deals in 2015. “The industry's growth rate plus the increase in investment activity will create more opportunities for attractive exits in the future.” According to the NCN Transaction Database, the average sales multiple for a Branded Food & Beverage acquisition increased from 1.7 in 2013 to 2.1 in 2014 to 2.4 in 2015; the average size of a Branded Food & Beverage company acquired increased from $121 million in 2013 to $134 million in 2014, to $163 million in 2015.

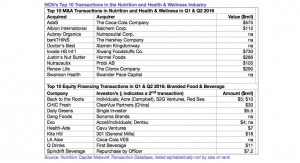

Boom In Equity Financings in Branded Food & Beverage

NCN recorded 69 equity investments in 2015 in Branded Food & Beverage (mostly natural and organic but also including functional and medical foods), more than doubling the 33 Branded Food & Beverage financings recorded in the whole of 2014. Highlights included Coca-Cola leading a $149 million round in juice company Suja; Kleiner Perkins, Campbell's Soup, Google Ventures and others investing $120 million in Juicero; and $50 million investments in coconut- and almond-themed beverage companies Harmless Harvest and Califia Farms, respectively.

While financings leveled off in Supplements and Nutritional Ingredients in 2015, perhaps due to uncertainties in the supplement industry, Technology segments continued to grab headlines in 2015.

Five Technology Segments Account for More Than Half of Industry Financings

The five Technology segments defined and tracked by NCN accounted for 63% or 207 of all 331 financing transactions recorded in 2015, with Delivery Service (78) and Apps & Information (53) leading the way. Out of 16 companies in the nutrition and health & wellness industry that raised more than $100 million each, eight were food delivery firms. Industry-wide, another 25 firms raised between $50-100 million in 2015.

“Developments in late 2015 saw a spike in the financing of delivery models in India and China, and some observers compare disruption in the food distribution space where grocery infrastructure is inconsistent or unreliable to the way cellular phones leap-frogged landlines in developing markets,” Mr. Ferrier observed. “The values these companies are commanding worldwide means their consumer reach will have to be a lot broader if most of them are going to survive.”

"While food delivery companies are focused on business disruption, the growth in apps has been consumer driven,” said Mike Dovbish, NCN executive director. “Technology companies that provide information, discovery and resources in health and wellness have proliferated, particularly in niche categories that provide more options for consumers hungry for health-related resources,” he said, citing April 2015’s $300-million investment in Jawbone as an example.

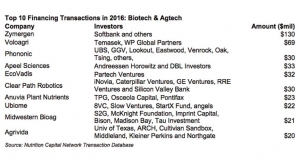

Biotech & Agtech Attract Investment

Robust financing in 2015 was also apparent in Biotech & Agtech, totaling 40 transactions in 2015 compared to 11 in 2014. Highlights included microbiome-focused Seres Therapeutics, food allergy treatment developer Aimmune Therapeutics, and the agricultural drone developers DJI and 3D Robotics, each raising between $50-100 million. Nutritional ingredient focused Pronutria and Gelesis raised $39 million and $22 million, respectively, and investments in a selection of agricultural technologies for efficiency or productivity were led by the Bill & Melinda Gates Foundation, among others.

NCN Success Rate

“We appreciate the high profile transactions that put the $260-billion U.S. nutrition and health & wellness industry in the mainstream financial press,” said Mr. Ferrier, “but the lifeblood of the industry, and the focus of our network are the smaller high-growth companies, particularly in branded products and ingredient science, where a broad base of entrepreneurs are devoting themselves to bringing health and wellness into the mainstream.” Of the 68 companies that presented business plans and capital requests at four NCN Investor Meetings in 2015, 14 have already obtained financing. Historically (2007 to mid-2015), 56% of NCN presenting companies have closed some kind of transaction.

Source: Nutrition Capital Network, NCN Transaction Database. Counts based on transactions detailed in the NCN Transaction Database© 2016 Nutrition Capital Network

Source: Nutrition Capital Network, NCN Transaction Database. Counts based on transactions detailed in the NCN Transaction Database© 2016 Nutrition Capital Network

Future NCN Investor Meetings in 2016

NCN XVIII, Metropolitan Pavilion, New York, April 20-21, 2016

NCN Europe III at Vitafoods, May 9, 2016, Geneva, Switzerland

NCN Ingredients & Technology Investor Meeting VIII at SupplySide West, October 5, 2016, Mandalay Bay Convention Center, Las Vegas

NCN XIX, San Francisco, date TBD, November 2016

(Other NCN events include: NCN at ExpoWest: Education session & PitchSlam VI, March 10, 2016; Vitafoods Venture Den I presented by Nutrition Capital Network on May 10 in Geneva; NCN at ExpoEast: Education session & PitchSlam VII, September 15, 2016, Baltimore; NCN Venture Tank II at SupplySide West, October 7)

“2015 was a record year for equity investments and acquisitions in the nutrition and health & wellness industry, and by no small margin,” said Grant Ferrier, NCN founder and CEO. “Venture investments more than doubled in agtech, Branded Food & Beverages, and food delivery; in the latter two categories, more than one deal a week was announced.”

Increase In Earlier-Stage Investments

Interest from big food companies, venture and private equity funds, and “cross-over” investors from technology and biotech all helped drive activity, but Mr. Ferrier also noted an increase in earlier stage investments by high net worth individuals, angel investors, former industry executives, crowdfunding, incubators, accelerators and other alternative financing models. “In 2015 we counted 40 equity investments of less than $2 million in branded products, more than the previous two years combined.”

Equity Financings Rise 61%, M&As Increase 29%

Overall transactions (i.e., acquisitions plus equity financings) in the nutrition and health & wellness industry totaled 558 in 2015, compared to annual totals of 382 in 2014 and 253 in 2013, according to the NCN Transaction Database, which tracks deals according to several industry segments, including supplements, natural & organic food, functional food, ingredients, retail & distribution, contract manufacturing, technology, natural personal care and household goods.

Equity financings accounted for 331 of total industry transactions in 2015, up 61% over the prior year, and more than $7 billion invested in deals for which the amount invested was available. Technology accounted for 207 or 63% of those equity financings but 69% of total value invested with 41 technology investments falling in the $50 million+ range.

Mergers and acquisitions (M&As) accounted for 224 of total industry transactions in 2015 compared to 168 in 2014, a 29% increase. Total transaction value of the top 10 listed deals in the food & beverage category was $7 billion.

“Strong brands command a high price,” said Mr. Ferrier, citing Krave, Vega, Applegate Farms, Kettle and Smart Balance as examples of top deals in 2015. “The industry's growth rate plus the increase in investment activity will create more opportunities for attractive exits in the future.” According to the NCN Transaction Database, the average sales multiple for a Branded Food & Beverage acquisition increased from 1.7 in 2013 to 2.1 in 2014 to 2.4 in 2015; the average size of a Branded Food & Beverage company acquired increased from $121 million in 2013 to $134 million in 2014, to $163 million in 2015.

Boom In Equity Financings in Branded Food & Beverage

NCN recorded 69 equity investments in 2015 in Branded Food & Beverage (mostly natural and organic but also including functional and medical foods), more than doubling the 33 Branded Food & Beverage financings recorded in the whole of 2014. Highlights included Coca-Cola leading a $149 million round in juice company Suja; Kleiner Perkins, Campbell's Soup, Google Ventures and others investing $120 million in Juicero; and $50 million investments in coconut- and almond-themed beverage companies Harmless Harvest and Califia Farms, respectively.

While financings leveled off in Supplements and Nutritional Ingredients in 2015, perhaps due to uncertainties in the supplement industry, Technology segments continued to grab headlines in 2015.

Five Technology Segments Account for More Than Half of Industry Financings

The five Technology segments defined and tracked by NCN accounted for 63% or 207 of all 331 financing transactions recorded in 2015, with Delivery Service (78) and Apps & Information (53) leading the way. Out of 16 companies in the nutrition and health & wellness industry that raised more than $100 million each, eight were food delivery firms. Industry-wide, another 25 firms raised between $50-100 million in 2015.

“Developments in late 2015 saw a spike in the financing of delivery models in India and China, and some observers compare disruption in the food distribution space where grocery infrastructure is inconsistent or unreliable to the way cellular phones leap-frogged landlines in developing markets,” Mr. Ferrier observed. “The values these companies are commanding worldwide means their consumer reach will have to be a lot broader if most of them are going to survive.”

"While food delivery companies are focused on business disruption, the growth in apps has been consumer driven,” said Mike Dovbish, NCN executive director. “Technology companies that provide information, discovery and resources in health and wellness have proliferated, particularly in niche categories that provide more options for consumers hungry for health-related resources,” he said, citing April 2015’s $300-million investment in Jawbone as an example.

Biotech & Agtech Attract Investment

Robust financing in 2015 was also apparent in Biotech & Agtech, totaling 40 transactions in 2015 compared to 11 in 2014. Highlights included microbiome-focused Seres Therapeutics, food allergy treatment developer Aimmune Therapeutics, and the agricultural drone developers DJI and 3D Robotics, each raising between $50-100 million. Nutritional ingredient focused Pronutria and Gelesis raised $39 million and $22 million, respectively, and investments in a selection of agricultural technologies for efficiency or productivity were led by the Bill & Melinda Gates Foundation, among others.

NCN Success Rate

“We appreciate the high profile transactions that put the $260-billion U.S. nutrition and health & wellness industry in the mainstream financial press,” said Mr. Ferrier, “but the lifeblood of the industry, and the focus of our network are the smaller high-growth companies, particularly in branded products and ingredient science, where a broad base of entrepreneurs are devoting themselves to bringing health and wellness into the mainstream.” Of the 68 companies that presented business plans and capital requests at four NCN Investor Meetings in 2015, 14 have already obtained financing. Historically (2007 to mid-2015), 56% of NCN presenting companies have closed some kind of transaction.

Source: Nutrition Capital Network, NCN Transaction Database. Counts based on transactions detailed in the NCN Transaction Database© 2016 Nutrition Capital Network

Source: Nutrition Capital Network, NCN Transaction Database. Counts based on transactions detailed in the NCN Transaction Database© 2016 Nutrition Capital Network

Future NCN Investor Meetings in 2016

NCN XVIII, Metropolitan Pavilion, New York, April 20-21, 2016

NCN Europe III at Vitafoods, May 9, 2016, Geneva, Switzerland

NCN Ingredients & Technology Investor Meeting VIII at SupplySide West, October 5, 2016, Mandalay Bay Convention Center, Las Vegas

NCN XIX, San Francisco, date TBD, November 2016

(Other NCN events include: NCN at ExpoWest: Education session & PitchSlam VI, March 10, 2016; Vitafoods Venture Den I presented by Nutrition Capital Network on May 10 in Geneva; NCN at ExpoEast: Education session & PitchSlam VII, September 15, 2016, Baltimore; NCN Venture Tank II at SupplySide West, October 7)