Dr. A. Elizabeth Sloan & Dr. Catherine Adams Hutt, Sloan Trends, Inc.07.01.15

Not surprisingly, the rising demand for more natural health solutions and “close-to-nature” ingredients is creating a myriad of new opportunities across a wide realm of nutraceutical product categories.

In 2013, herbs/botanical supplements enjoyed the highest growth rate since the late 1990s, with sales up 7.1% to $6.4 billion, the tenth year of consecutive growth. Plant oil supplement sales reached $312 million, while the $140 million bee product category grew 7.9% (Nutrition Business Journal).

Herbs/botanicals have been a driving force in the penetration of natural remedies into the over-the-counter (OTC) drug category. For example, among the top 10 best-selling sleep aids, MidNite PM is formulated with melatonin and a blend of lavender, lemon balm and chamomile; Alteril contains L-tryptophan, melatonin and valerian.

The naturally-focused $1.2 billion homeopathic supplement category grew 5.1% in 2014, Ayurvedic supplements 5.8%, and Chinese herbs 3.9%, according to Nutrition Business Journal’s 2015 data sheets.

More than a decade of ethnological research by the Hartman Group confirms that core users are cutting back on the number of supplements they take daily because they believe the quality/benefits of nutrients in foods are best and because they have pervasive doubts about the bioavailability of even the highest quality supplement brands (Hartman, Reimagining Health + Nutrition, 2010, 2013).

Since 2013, there has been a dramatic shift in the balance of consumers who believe supplements are necessary for good nutrition vs. those who feel their needs can be met by food alone (51% vs. 49% currently compared to 59% vs. 41% in 2012), according to the 2014 Gallup Study of Nutrient Knowledge & Consumption.”

Not surprisingly, whole food supplements were one of the fastest growing supplement sectors in 2014, with sales projected to grow from $1.7 billion to $2.7 billion in 2017 (NBJ, 2015).

Fruit/vegetable supplement sales topped $117 million in 2014, after three years of double-digit growth. Superfood juice supplements posted strong sales: noni $229 million, mangosteen $176 million and goji juice jumped 10.4% to $119 million (NBJ, 2015).

Green tea supplement sales topped $135 million in 2014, green foods $103 million, mushrooms $32 million, and hops $15 million (NBJ, 2015).

The naturally functional movement has also moved center stage in the food and beverage business. Half (51%) of consumers prefer to get nutrients/health benefits that are naturally occurring in foods vs. fortification (IFIC, Functional Food Consumer Survey, 2013).

Three-quarters of consumers believe that some foods contain active components that can help manage current health issues, such as digestion; 65% believe some foods can reduce the risk of disease and improve long-term health. More than half (54%) think food can be used to reduce their use of some drugs/medical therapies (HealthFocus, 2013).

While fortified/functional foods and drinks led global growth of healthy foods in 2013—up 10%—naturally healthy/naturally nutritious foods were a close second, +8% (Euromonitor 2014 Health and Wellness Performance Overview, March 2014).

Another significant opportunity involves the penetration of food and plant/botanical-based ingredients into non-food based categories (e.g., the $14.3 billion natural personal care sector (NBJ, July 2014).

NBJ estimated the U.S. nutritional cosmetic market at $17.2 billion in 2013. More than half (56%) of facial skin care users are interested in products that are made from natural food ingredients (e.g., ginger or olive), according to Mintel’s Facial Skincare – U.S., 2014.

Sales of all-natural pet foods jumped 12% in 2014. One-quarter of dog owners gave their pet a nutraceutical treat last year; one in five gave their dog an omega-3 supplement; and one in 10 a calming treat, reported Packaged Facts’ U.S. Pet Outlook 2014-15.

Market Potential

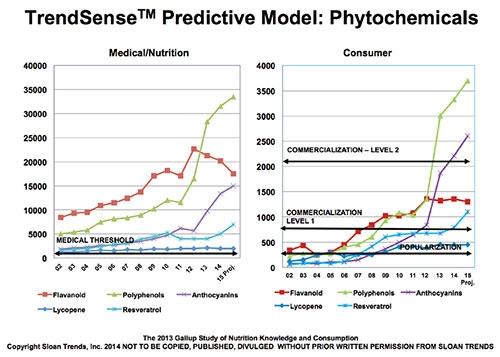

According to Sloan Trend’s TrendSense model, flavonoids/flavanols and polyphenols were the first phytonutrients to reach Mass Market status, back in 2007-08.

The marketability of polyphenols continues to escalate as a large Level 2 Mass Market, driven by a seven-fold increase in medical research activity over the past 13 years. Six in 10 (62%) adults are aware of polyphenols; 21% are making a strong effort to get more.

Until 2012, flavonoids were also on the fast track with new research activity nearly tripling over the previous 10 years—until Mars cut back its research funding and the CocoaVia cocoa flavonol ingredient program. Despite more than 200 well-executed clinical studies, flavonoids have settled into a stable, but smaller Level 1 Mass Market opportunity.

Cocoa flavanols are best known for supporting healthy circulation, a fast accelerating Level 3 Mass Market. According to TrendSense, antioxidants, energy/performance, and heart health are the top health linkages associated with circulation. The Gallup 2012 Circulatory Health Study confirmed that two-thirds of adults are concerned about circulation.

Anthocyanins, prevalent in tart cherries and other red foods, hold great promise—skyrocketing to a Level 2 Mass Market in 2013-14.

Resveratrol has finally become a mainstream Mass Market; 24% of consumers are aware of resveratrol, per Gallup. Although relatively small in supplement sales at $44 million, resveratrol sales jumped 20.8% in 2014, reported NBJ.

Lycopene, lutein, and green tea (the latter two not shown) remain strong/stable but lackluster natural ingredient markets in specialty/health food channels and among very health conscious/condition-specific shoppers. Half of consumers are aware of green tea, and 29% lutein, per Gallup.

Antioxidants, which are a Mega Level market status, continue to accelerate and are the driving force behind these phytonutrients. Half (51%) of adults are making a strong effort to get more antioxidants, 32% more natural antioxidants, per Gallup.

According to TrendSense, the market for the terms “phytochemical” and “phytonutrients” has given way to the individual scientific names (e.g., flavonoids or lutein).

Although still in the Emerging Phase, we believe that hydroxytyrosol, astaxanthan, and pterostilbene will be strong scientifically supportable phytonutrient opportunities. Hydroxytyrosol enjoys an EFSA approved health claim in Europe. Less than 5% of consumers are aware of these ingredients, per Gallup.

Growth Potential: Natural Solutions

With one-third of consumers making a strong effort to eat more foods naturally “rich-in” nutrients, per Gallup, food/beverage marketers would be wise to tout good/excellent source claims, particularly on breakfast/morning snack products when the demand for nutrients is highest.

According to IRI’s 2014 New Product Pacesetter Report, 39% of the new best-selling foods/beverages touted a natural/organic claim, 36% real fruit/real fruit health benefits, 22% enriched with vitamins/minerals, and 14% real vegetables/real vegetable health benefits.

Three-quarters of consumers prefer to get their fiber from foods, 72% protein, 72% antioxidants, 47% calcium, 45% iron, 44% omega-3s and 43% probiotics, according to the Hartman Group (2013).

Dietary Supplements

Four in 10 (42%) consumers prefer to get vitamin D from supplements, 41% omega-3s, 36% iron, 31% calcium, 33% probiotics and 31% calcium, according to Hartman.

Supplement and ingredient marketers should continue to look for innovative, naturally connected ingredients and broaden their scope in terms of applicable product categories.

Dr. A. Elizabeth Sloan & Dr. Catherine Adams Hutt

Sloan Trends, Inc.

Dr. A. Elizabeth Sloan and Dr. Catherine Adams Hutt are president and chief scientific and regulatory officer, respectively, of Sloan Trends, Inc., Escondido, CA, a 20-year-old consulting firm that offers trend interpretation/predictions; identifies emerging high potential opportunities; and provides strategic counsel on issues and regulatory claims guidance for food/beverage, supplement and pharmaceutical marketers. For more information: E-mail: lizsloan@sloantrend.com; Website: www.sloantrend.com

In 2013, herbs/botanical supplements enjoyed the highest growth rate since the late 1990s, with sales up 7.1% to $6.4 billion, the tenth year of consecutive growth. Plant oil supplement sales reached $312 million, while the $140 million bee product category grew 7.9% (Nutrition Business Journal).

Herbs/botanicals have been a driving force in the penetration of natural remedies into the over-the-counter (OTC) drug category. For example, among the top 10 best-selling sleep aids, MidNite PM is formulated with melatonin and a blend of lavender, lemon balm and chamomile; Alteril contains L-tryptophan, melatonin and valerian.

The naturally-focused $1.2 billion homeopathic supplement category grew 5.1% in 2014, Ayurvedic supplements 5.8%, and Chinese herbs 3.9%, according to Nutrition Business Journal’s 2015 data sheets.

More than a decade of ethnological research by the Hartman Group confirms that core users are cutting back on the number of supplements they take daily because they believe the quality/benefits of nutrients in foods are best and because they have pervasive doubts about the bioavailability of even the highest quality supplement brands (Hartman, Reimagining Health + Nutrition, 2010, 2013).

Since 2013, there has been a dramatic shift in the balance of consumers who believe supplements are necessary for good nutrition vs. those who feel their needs can be met by food alone (51% vs. 49% currently compared to 59% vs. 41% in 2012), according to the 2014 Gallup Study of Nutrient Knowledge & Consumption.”

Not surprisingly, whole food supplements were one of the fastest growing supplement sectors in 2014, with sales projected to grow from $1.7 billion to $2.7 billion in 2017 (NBJ, 2015).

Fruit/vegetable supplement sales topped $117 million in 2014, after three years of double-digit growth. Superfood juice supplements posted strong sales: noni $229 million, mangosteen $176 million and goji juice jumped 10.4% to $119 million (NBJ, 2015).

Green tea supplement sales topped $135 million in 2014, green foods $103 million, mushrooms $32 million, and hops $15 million (NBJ, 2015).

The naturally functional movement has also moved center stage in the food and beverage business. Half (51%) of consumers prefer to get nutrients/health benefits that are naturally occurring in foods vs. fortification (IFIC, Functional Food Consumer Survey, 2013).

Three-quarters of consumers believe that some foods contain active components that can help manage current health issues, such as digestion; 65% believe some foods can reduce the risk of disease and improve long-term health. More than half (54%) think food can be used to reduce their use of some drugs/medical therapies (HealthFocus, 2013).

While fortified/functional foods and drinks led global growth of healthy foods in 2013—up 10%—naturally healthy/naturally nutritious foods were a close second, +8% (Euromonitor 2014 Health and Wellness Performance Overview, March 2014).

Another significant opportunity involves the penetration of food and plant/botanical-based ingredients into non-food based categories (e.g., the $14.3 billion natural personal care sector (NBJ, July 2014).

NBJ estimated the U.S. nutritional cosmetic market at $17.2 billion in 2013. More than half (56%) of facial skin care users are interested in products that are made from natural food ingredients (e.g., ginger or olive), according to Mintel’s Facial Skincare – U.S., 2014.

Sales of all-natural pet foods jumped 12% in 2014. One-quarter of dog owners gave their pet a nutraceutical treat last year; one in five gave their dog an omega-3 supplement; and one in 10 a calming treat, reported Packaged Facts’ U.S. Pet Outlook 2014-15.

Market Potential

According to Sloan Trend’s TrendSense model, flavonoids/flavanols and polyphenols were the first phytonutrients to reach Mass Market status, back in 2007-08.

The marketability of polyphenols continues to escalate as a large Level 2 Mass Market, driven by a seven-fold increase in medical research activity over the past 13 years. Six in 10 (62%) adults are aware of polyphenols; 21% are making a strong effort to get more.

Until 2012, flavonoids were also on the fast track with new research activity nearly tripling over the previous 10 years—until Mars cut back its research funding and the CocoaVia cocoa flavonol ingredient program. Despite more than 200 well-executed clinical studies, flavonoids have settled into a stable, but smaller Level 1 Mass Market opportunity.

Cocoa flavanols are best known for supporting healthy circulation, a fast accelerating Level 3 Mass Market. According to TrendSense, antioxidants, energy/performance, and heart health are the top health linkages associated with circulation. The Gallup 2012 Circulatory Health Study confirmed that two-thirds of adults are concerned about circulation.

Anthocyanins, prevalent in tart cherries and other red foods, hold great promise—skyrocketing to a Level 2 Mass Market in 2013-14.

Resveratrol has finally become a mainstream Mass Market; 24% of consumers are aware of resveratrol, per Gallup. Although relatively small in supplement sales at $44 million, resveratrol sales jumped 20.8% in 2014, reported NBJ.

Lycopene, lutein, and green tea (the latter two not shown) remain strong/stable but lackluster natural ingredient markets in specialty/health food channels and among very health conscious/condition-specific shoppers. Half of consumers are aware of green tea, and 29% lutein, per Gallup.

Antioxidants, which are a Mega Level market status, continue to accelerate and are the driving force behind these phytonutrients. Half (51%) of adults are making a strong effort to get more antioxidants, 32% more natural antioxidants, per Gallup.

According to TrendSense, the market for the terms “phytochemical” and “phytonutrients” has given way to the individual scientific names (e.g., flavonoids or lutein).

Although still in the Emerging Phase, we believe that hydroxytyrosol, astaxanthan, and pterostilbene will be strong scientifically supportable phytonutrient opportunities. Hydroxytyrosol enjoys an EFSA approved health claim in Europe. Less than 5% of consumers are aware of these ingredients, per Gallup.

Growth Potential: Natural Solutions

- The projected fastest growing categories in 2015 in the $36 billion condition-specific supplement sector are gastrointestinal health (+14.8%), insomnia (+13.2%), liver/detox (+12.6%) and anti-aging (9%) (NBJ, April 2015).

- Herbals/botanicals are projected to drive growth in the whole food supplement category with sales approaching $1.1 billion by 2018, followed by whole food vitamins ($800 million by 2018), specialty supplements ($450 million) and meal supplements ($200 million) (NBJ, March 2015).

- Horehound was the best-selling herbal supplement in mass channels in 2013 followed by yohimbe, cranberry, black cohosh, senna, cinnamon, flaxseed/oil, echinacea, valerian and saw palmetto; overall mass herbal sales jumped 9.4% (HerbalGram 2014).

- Turmeric, followed by grass (wheat and/or barley), flaxseed/oil, aloe vera, spirulina, blue green algae, milk thistle, elderberry, echinacea, mace and saw palmetto were the top herbal supplements in the natural channel, up 9.9% overall in 2013 (HerbalGram 2014).

- Combination herbs account for 6% of the anti-aging supplement market (NBJ, April 2015).

- All-natural, botanical/herbal, antioxidant and vitamin/mineral fortified were among the top global skin care claims in 2014 (Mintel, Global Skincare Category Insights, 2014).

- Three in 10 consumers classify their “diet lifestyle” as “whole foods” followed by “minimally processed” at 24% (NBJ, Diet Tribes, March 2015).

- If they had a medical condition, 80% of adults would use specific foods to help manage this condition as part of a treatment (HealthFocus, 2013).

- Functional foods are projected to grow from $51 billion in 2014 to $66.8 billion by 2017 (NBJ, April 2015).

- Energy boosting, food intolerance, general well-being, digestive health and beauty were among the fastest growing new food positionings globally over the past five years, according to Euromonitor; general well-being, weight management, digestive health, energy boosting and endurance remain the top five best-selling positionings.

With one-third of consumers making a strong effort to eat more foods naturally “rich-in” nutrients, per Gallup, food/beverage marketers would be wise to tout good/excellent source claims, particularly on breakfast/morning snack products when the demand for nutrients is highest.

According to IRI’s 2014 New Product Pacesetter Report, 39% of the new best-selling foods/beverages touted a natural/organic claim, 36% real fruit/real fruit health benefits, 22% enriched with vitamins/minerals, and 14% real vegetables/real vegetable health benefits.

Three-quarters of consumers prefer to get their fiber from foods, 72% protein, 72% antioxidants, 47% calcium, 45% iron, 44% omega-3s and 43% probiotics, according to the Hartman Group (2013).

Dietary Supplements

Four in 10 (42%) consumers prefer to get vitamin D from supplements, 41% omega-3s, 36% iron, 31% calcium, 33% probiotics and 31% calcium, according to Hartman.

Supplement and ingredient marketers should continue to look for innovative, naturally connected ingredients and broaden their scope in terms of applicable product categories.

Dr. A. Elizabeth Sloan & Dr. Catherine Adams Hutt

Sloan Trends, Inc.

Dr. A. Elizabeth Sloan and Dr. Catherine Adams Hutt are president and chief scientific and regulatory officer, respectively, of Sloan Trends, Inc., Escondido, CA, a 20-year-old consulting firm that offers trend interpretation/predictions; identifies emerging high potential opportunities; and provides strategic counsel on issues and regulatory claims guidance for food/beverage, supplement and pharmaceutical marketers. For more information: E-mail: lizsloan@sloantrend.com; Website: www.sloantrend.com