Diana Cowland, Health and Wellness Analyst, Euromonitor01.10.13

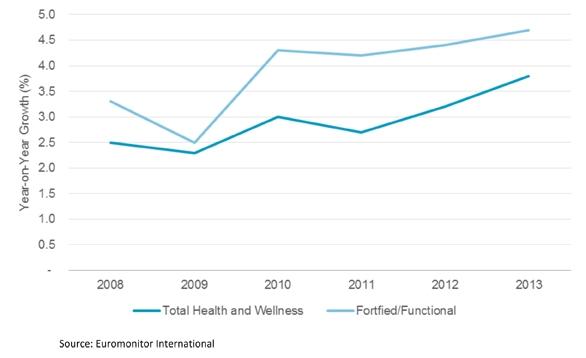

Euromonitor International predicts that in 2013 an additional $27 billion, in constant terms, will be added to the value of health and wellness, just under half of which will stem from fortified/functional products. Strong recovery of the global health and wellness market is continuing, with sales recording a constant 3% value rise in 2012 excluding inflation (equivalent to growth of 7% in current terms). Products offering specific health benefits, such as fortified/functional, are driving value sales, with a constant rise of 4% in 2012. In comparison, globally conventional packaged food saw constant value growth of just 2% in the same year.

Healthy Convenience on the Rise

Forty of the top 100 health and wellness brands saw their sales rise by more than $100 million in 2011, a clear statement that combining four key factors (health, convenience, fashionable packaging and affordable price) is a winning strategy behind successful health and wellness developments. These factors played a key role in the success of products such as naturally healthy ready-to-drink (RTD) green tea. Overtaking sales of traditional green tea, the RTD format has spread from Asia across the world and is expected to see an annual value growth rate of 10% in 2013.

Year-on-Year Value Growth of Total Health and Wellness vs. Fortified/Functional Products 2008-2013

According to the new Global Burden of Disease report, for the first time, diseases associated with obesity are now a greater global health burden than those associated with lack of nutrition. Despite numerous attempts to curb the growing obesity epidemic, the obese and overweight population is on the rise, crossing the 70% benchmark in Mexico, Venezuela, Australia and Egypt (among over 15-year-old populations). Long-term solutions for calorie reduction via healthy lifestyle changes are becoming a necessity and hugely benefiting global sales of weight management-positioned food and beverages, already worth a staggering $163 billion in 2012.

Fat reduction is no longer sufficient on its own. The growing fashion for natural and less conventional slimming solutions has seen companies innovate further, this time with the natural high intensity sweetener, stevia. Products sweetened with stevia are thriving in the U.S. and since its authorization in the EU in December 2011, an array of new products have hit the shelves, opening up the chase for the first global brand. Coca-Cola, which clearly sees a strong future for the sweetener, is part of this race. The company has already introduced stevia into Sprite in Europe and more recently into Glacéau VitaminWater in the U.K. So, it would not be surprising to see a stevia sweetened Coca-Cola variant on the horizon for 2013.

Innovation: At the Heart of Health & Wellness

Innovation and product reformulation are at the heart of health and wellness. But, science continues to outpace the regulators and legislative constraints are proving hard for health and wellness players. Restrictions continue to tighten across the world and while new laws—especially the European Commission’s list of 224 general health claims, which came into force in December 2012—offer opportunities industry-wide, they have also finally closed the door on many long-used health claims.

Probiotics, with no approved claims in the EU, are among the most adversely affected, and Western Europe is expected to witness the fourth consecutive year of sales decline in constant terms in 2013 for pro-/prebiotic yogurt, after years of spectacular growth prior to 2008. Yet, while this negative performance pulled the global performance of pro-/prebiotic yogurt down, growth still remained at 6% in 2012, with sales set to grow by a further 7% in 2013.

Finally, nutrigenomics or personalized nutrition, whereby food scientists seek to treat chronic health conditions such as cardiovascular disease, diabetes, obesity and Alzheimer’s disease through diet, is a step closer. Leading players such as Nestlé, PepsiCo and Danone have heavily invested in institutes of nutrition, research and development. As the movement toward prevention grows, it is starting to attract the attention of the big pharmaceutical players with substantial investments likely to follow.

Euromonitor International predicts that steady real term growth in current prices is expected to continue until 2017, with global health and wellness sales on the way to hit a record high of $1 trillion by 2017.

——

The ideas and opinions expressed in this article are those of the author and do not necessarily reflect views held by Nutraceuticals World.

Healthy Convenience on the Rise

Forty of the top 100 health and wellness brands saw their sales rise by more than $100 million in 2011, a clear statement that combining four key factors (health, convenience, fashionable packaging and affordable price) is a winning strategy behind successful health and wellness developments. These factors played a key role in the success of products such as naturally healthy ready-to-drink (RTD) green tea. Overtaking sales of traditional green tea, the RTD format has spread from Asia across the world and is expected to see an annual value growth rate of 10% in 2013.

Year-on-Year Value Growth of Total Health and Wellness vs. Fortified/Functional Products 2008-2013

According to the new Global Burden of Disease report, for the first time, diseases associated with obesity are now a greater global health burden than those associated with lack of nutrition. Despite numerous attempts to curb the growing obesity epidemic, the obese and overweight population is on the rise, crossing the 70% benchmark in Mexico, Venezuela, Australia and Egypt (among over 15-year-old populations). Long-term solutions for calorie reduction via healthy lifestyle changes are becoming a necessity and hugely benefiting global sales of weight management-positioned food and beverages, already worth a staggering $163 billion in 2012.

Fat reduction is no longer sufficient on its own. The growing fashion for natural and less conventional slimming solutions has seen companies innovate further, this time with the natural high intensity sweetener, stevia. Products sweetened with stevia are thriving in the U.S. and since its authorization in the EU in December 2011, an array of new products have hit the shelves, opening up the chase for the first global brand. Coca-Cola, which clearly sees a strong future for the sweetener, is part of this race. The company has already introduced stevia into Sprite in Europe and more recently into Glacéau VitaminWater in the U.K. So, it would not be surprising to see a stevia sweetened Coca-Cola variant on the horizon for 2013.

Innovation: At the Heart of Health & Wellness

Innovation and product reformulation are at the heart of health and wellness. But, science continues to outpace the regulators and legislative constraints are proving hard for health and wellness players. Restrictions continue to tighten across the world and while new laws—especially the European Commission’s list of 224 general health claims, which came into force in December 2012—offer opportunities industry-wide, they have also finally closed the door on many long-used health claims.

Probiotics, with no approved claims in the EU, are among the most adversely affected, and Western Europe is expected to witness the fourth consecutive year of sales decline in constant terms in 2013 for pro-/prebiotic yogurt, after years of spectacular growth prior to 2008. Yet, while this negative performance pulled the global performance of pro-/prebiotic yogurt down, growth still remained at 6% in 2012, with sales set to grow by a further 7% in 2013.

Finally, nutrigenomics or personalized nutrition, whereby food scientists seek to treat chronic health conditions such as cardiovascular disease, diabetes, obesity and Alzheimer’s disease through diet, is a step closer. Leading players such as Nestlé, PepsiCo and Danone have heavily invested in institutes of nutrition, research and development. As the movement toward prevention grows, it is starting to attract the attention of the big pharmaceutical players with substantial investments likely to follow.

Euromonitor International predicts that steady real term growth in current prices is expected to continue until 2017, with global health and wellness sales on the way to hit a record high of $1 trillion by 2017.

——

The ideas and opinions expressed in this article are those of the author and do not necessarily reflect views held by Nutraceuticals World.